Retirement planning for women

You've probably heard about the wage gap. On average, women earn about 82 cents for every dollar earned by men.

This number hasn't changed much in the past two decades, although there are indications that the wage gap is narrowing among younger workers.

How unique challenges impact retirement planning for women

Women face unique challenges when it comes to retirement planning. The wage gap represents one significant challenge for women. Another is that women are more likely to take time away from work to raise a child or care for an aging parent, which has the potential to limit their total earnings, as well as their Social Security benefits in retirement. This can be especially challenging because women on average have a life expectancy that's longer than men, meaning it's critical to have retirement income for a longer duration.

According to a recent survey by the Teachers Insurance and Annuity Association of America, only 19% of women felt confident about retiring without running out of money—compared to 35% of men. Women consistently trailed men by a significant margin in various retirement confidence surveys.

Retirement readiness

Understanding these challenges—and others—can help women prepare for retirement early and protect their savings across their careers and other key life moments. Working with an advisor or banker can boost confidence and provide a strong sounding board for ideas that can help close the retirement confidence gap.

Here are some additional stats on women, wealth and financial health.

Common challenges women face

- Life expectancy: Women on average live to age 79, while men live to age 73. These extra years of life mean an increased need for retirement income.

- Lifetime earnings: Women on average earn 21% less than men over a lifetime, which can result in less retirement savings and lower Social Security benefits.

- Caregiving responsibilities: 61% of caregivers are women. This often requires reduced work hours or breaks from careers.

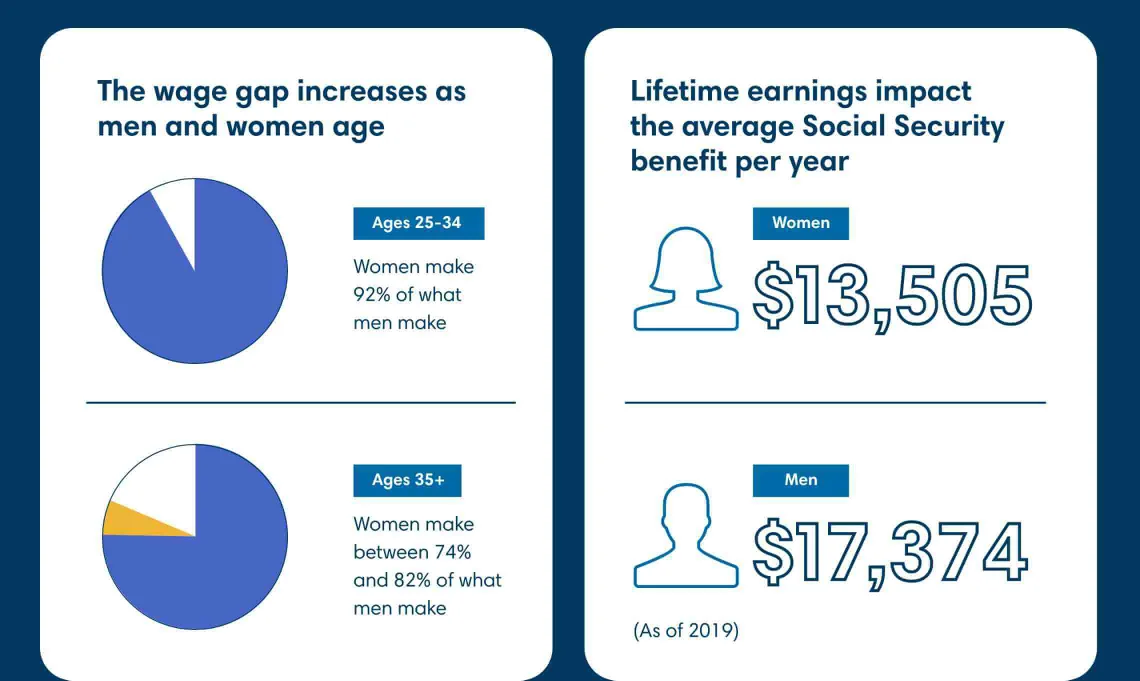

The wage gap increases as men and women age

- Ages 25 to 34: Women make 92% of what men make.

- Ages 35+: Women make between 74% and 82% of what men make.

Lifetime earnings impact the average Social Security benefit per year (as of 2019)

- Women: $13,505

- Men: $17,374

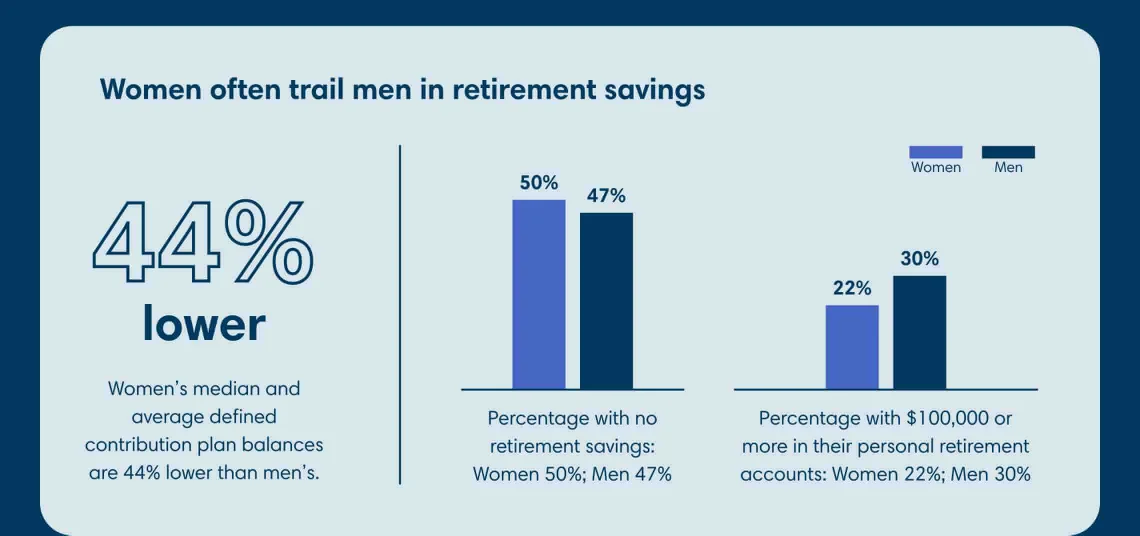

Women often trail men in retirement savings

- 44% lower: Women's median and average defined contribution plan balances are 44% lower than men's.

- Percentage with no retirement savings: Women 50%; men 47%

- Percentage with $100,000 or more in their personal retirement accounts: Women 22%; men 30%

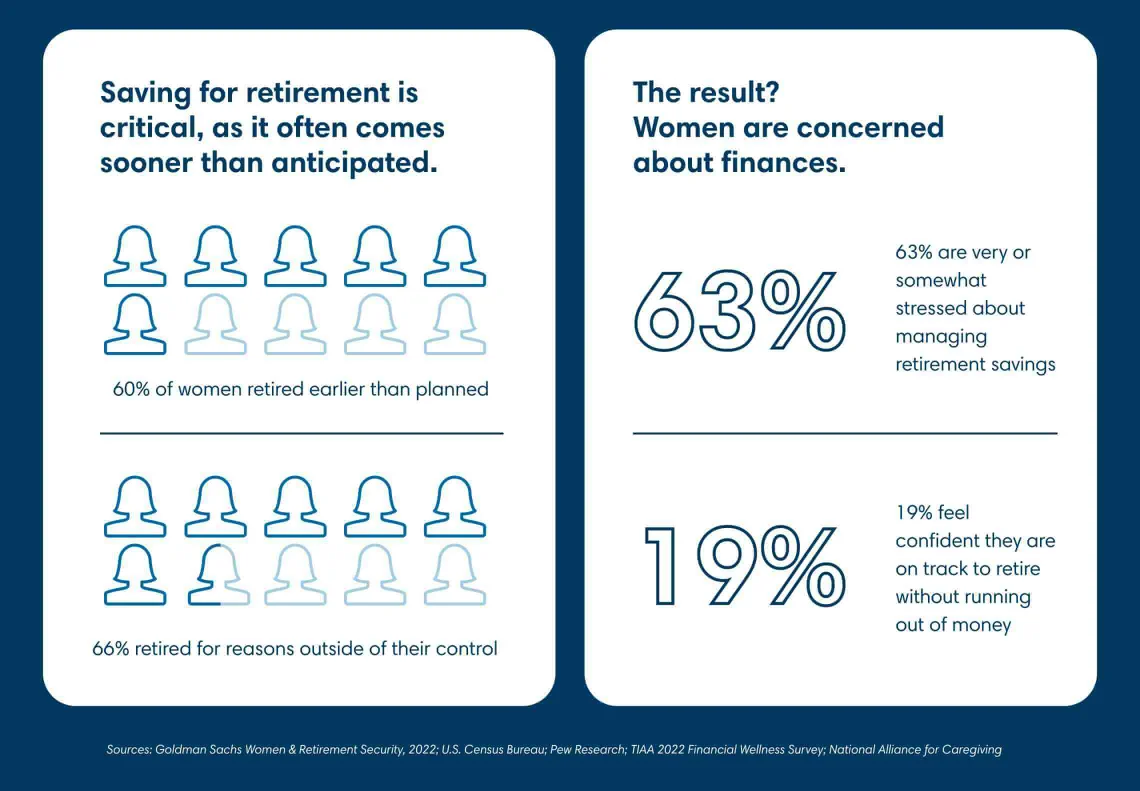

Saving for retirement is critical, as it often comes sooner than anticipated

- 60% of women retired earlier than planned.

- 66% retired for reasons outside of their control.

The result? Women are concerned about finances

- 63% are very or somewhat stressed about managing retirement savings.

- 19% feel confident they're on track to retire without running out of money.

Sources

- Goldman Sachs Women & Retirement Security, 2022

- US Census Bureau; Pew Research; TIAA 2022 Financial Wellness Survey

- National Alliance for Caregiving

Facing challenges head on

Addressing the challenges women face is essential to ensuring a secure and comfortable retirement. Take action to build your retirement plan. Learn more about the basics of retirement income.