How much life insurance do I need?

If you've reached a stage where you have more discretionary income than in the past, you may be ready to start investing more aggressively for your future. IRAs, 401(k) plans and taxable investment accounts are tactics you've probably considered. But what about life insurance?

You may find that life insurance can include benefits that go beyond simply providing for your beneficiaries in the event of your death.

Why consider life insurance?

Even at the beginning of your financial journey, life insurance can be a foundational component of a well-built investment strategy. So where should you start?

There are many types of life insurance available, but there are also several misconceptions about the importance of life insurance. In fact, 46% of millennials are confused about the specifics surrounding life insurance, leading many to hold off on buying a policy.

"Think of life insurance as the foundation of your financial house," says Kelly Sullivan, manager of Life Insurance Sales at First Citizens. "If you don't have this coverage, everything else falls apart if something happens to you because it's income replacement for those you leave behind."

To make the process easier and help ensure you're getting the right type of life insurance for your needs, ask yourself the following questions.

1When should I buy life insurance?

One of the biggest reasons people don't buy life insurance is that funds are allocated toward a death benefit instead of an investment account they can access later in life. However, this notion isn't entirely true.

Life insurance can offer you some living benefits in the case of chronic or terminal illness. Because chronic diseases account for a majority of illness, disability and death in the US, having a life insurance policy can prepare you financially if you face such an illness in the future.

You may be introduced to life insurance when your employer offers you a group life insurance policy as part of your benefits package. It's easy to opt in to this type of policy and take a set-it-and-forget-it approach to your coverage. However, it may not be for the amount you really need to protect yourself and your loved ones—and if you leave your employer, your life insurance policy typically doesn't come with you.

"While group policies may seem convenient, you have to remember that the coverage is designed to work for everyone in the group—even if they have completely different financial or medical situations," Sullivan notes. "But a good life insurance policy isn't one size fits all. Your coverage should account for your personal situation to make sure you aren't overinsured or underinsured."

For example, you typically don't need as much life insurance when you're single because you don't have a spouse or children relying on your future income to cover a mortgage and college expenses. Sullivan says buying a basic term life insurance policy that can be used as an emergency fund is a good place to start.

But for many people, getting married, buying a house and having a baby can all be life events that make buying life insurance a priority. Having life insurance is the best way to ensure your loved ones have the money they need in case you die.

2How much life insurance do I need?

There are two ways to determine how much life insurance you need. Remember, as your family grows and your financial liabilities increase, this will need to be recalculated.

The income-based rule of thumb formula says you should get a policy worth roughly 10 times your annual salary before taxes and other paycheck deductions. When you're single and just starting your career, your salary and liabilities will be lower than when you're in the middle of your career or close to retirement. This is why you can take out multiple life insurance policies throughout your career to ensure you always have enough coverage.

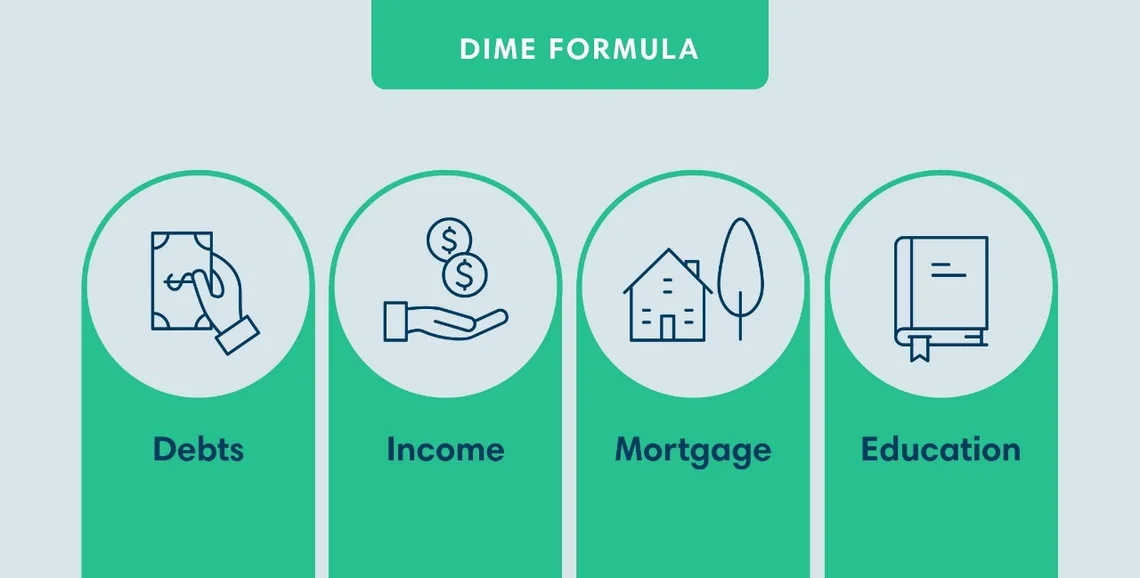

You can also use the DIME formula of debts, income, mortgage and education.

- Debts: Add up all loan balances except for mortgages.

- Income: Multiply your annual income by the number of years you think your dependents will need financial support.

- Mortgage: Determine how much you owe on your home, including any second mortgages or home equity loans or lines of credit.

- Education: Estimate the cost of paying for higher education for your children.

This may give a more accurate estimate of how much your family will need for essential costs but doesn't include any financial costs for healthcare and day-to-day living expenses.

3How do I choose which life insurance policies to use?

As you consider how much life insurance money you need, you'll also want to evaluate what type of life insurance fits your needs. The most common are term and permanent, or whole life insurance. You'll pay a monthly or annual premium for each insurance policy. Companies can base their premium rates on a variety of factors, including your age, gender and health.

Term life insurance policies are set for a specified time period—typically between 10 and 30 years—and premiums tend to be lower. These policies are good if you have a limited budget, want to ensure there's money to pay for your children's college education or pay down debt, or want to be able to convert to a permanent life insurance policy without a medical exam.

Here are a few types of term insurance.

- Convertible term insurance: This type of insurance can be converted to a permanent whole or universal life insurance policy without a medical exam, which helps guarantee insurance coverage even if your health deteriorates later in life.

- Decreasing term insurance: This renewable life insurance—which has a death benefit that gets smaller each year—is often purchased as a way to protect personal assets.

- Renewable term insurance: This is a 1-year policy that's ideal for young professionals who want a low-cost, flexible premium and no required medical exam.

Permanent or whole life insurance stays with you until you die or stop paying the premium. While premiums are more expensive, the policy accumulates cash value that you can use as a source of loans or cash. However, it will reduce the policy's death benefit when used this way.

Meanwhile, universal life insurance has flexible premiums and a cash-value component that earns interest. Unlike term and whole life, universal life insurance premiums can be adjusted over time and designed with a level death benefit or an increasing death benefit.

Like universal life, variable life policies allow the cash value portion to be invested in stocks, bonds and money market mutual funds so you can increase the value of your policy. However, your financial risk increases using this method. If your investments perform poorly, your cash value and death benefits may decrease.

4How often should I reevaluate my life insurance policies?

Sullivan says it's important to remember that your life insurance needs will evolve over time. As your net worth grows and your lifestyle changes, so do your insurance needs.

"I recommend reviewing your policies every 2 to 3 years at a minimum," she says. "It's important to make sure that what you have in place always covers all of your needs."

Help ensure your family is protected

We can help you and your loved ones stay protected for the future with life insurance that's right for you.