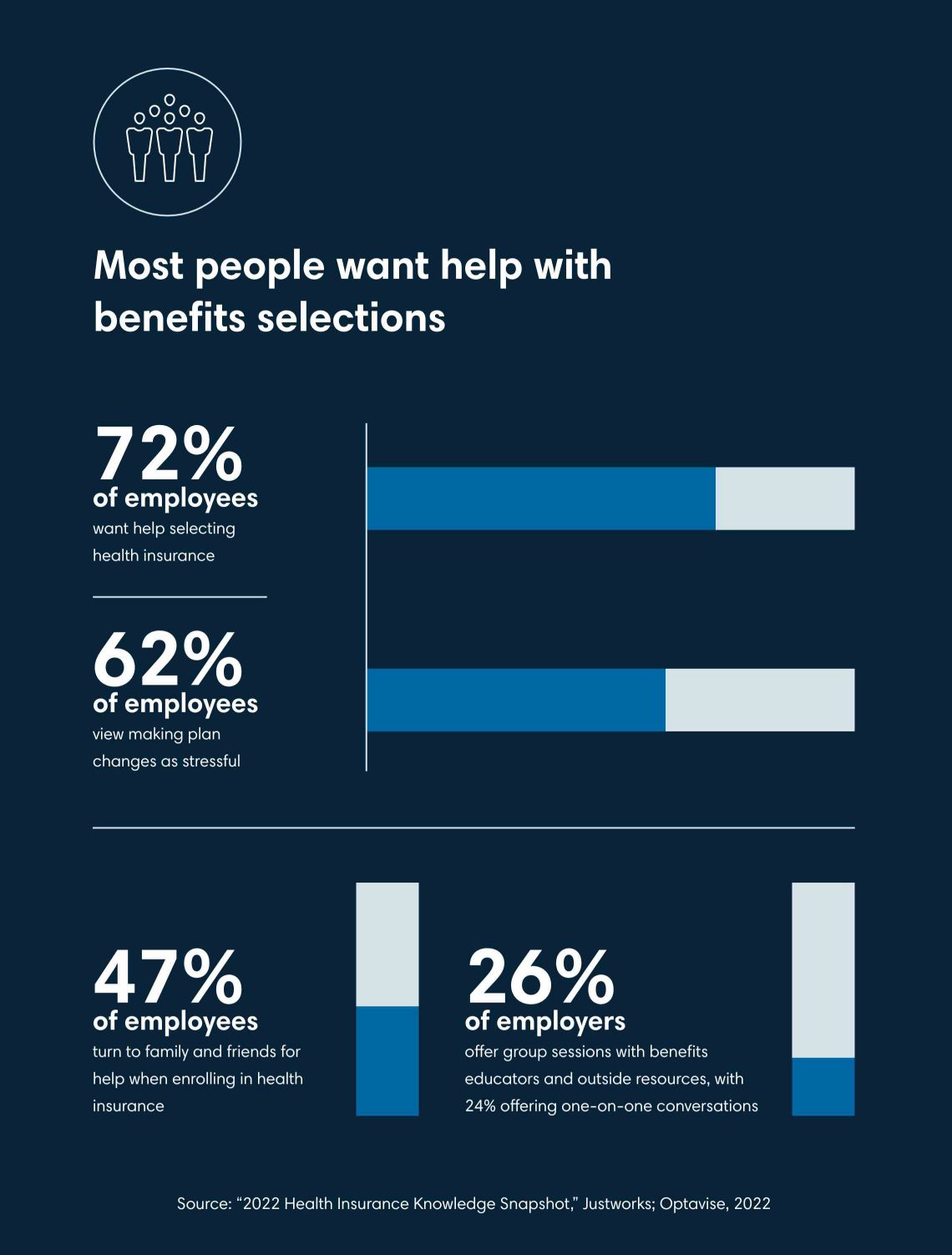

How to create a solid open enrollment benefits strategy

Open enrollment season is the time to make sure your benefits package aligns with what's important—and necessary—in your life.

According to First Citizens Wealth Planning Strategist Nate Harris and Life Insurance Sales Manager Kelly Sullivan, work benefits can also be an important part of your overall financial plan. Here, they cover some questions to answer as you make important decisions about your benefits.

Open enrollment basics

Open enrollment typically occurs during the end of the year—typically October through December—when you can enroll in benefits at work or make changes to your existing plans. The window is only open for a few weeks, though, so it's a good idea to know what you'll be updating before the time comes.

"I'm a planner, so I'm always going to bring everything back to having a holistic, comprehensive financial plan," Harris says. In other words, make sure all pieces of your finances work together so you make the most appropriate selections during open enrollment time.

Here are some questions to ask yourself to get started.

What's your short-term financial situation?

Your specific needs—not the forces of the economy or the markets—should drive your selections during open enrollment for workplace benefits, Sullivan and Harris say. Both cite emergency savings as a key measure. Can you afford to choose benefits that will be deducted from your take-home pay, or do you need more cash on hand with each paycheck?

"Situations not covered by benefits can happen fast, so you need a safety net to fall back on," Sullivan notes. If you already have an emergency savings account, make sure to regularly fund it. "You'll want to have savings set aside exclusively for use in an emergency," she says.

While you may not think of an emergency fund as a workplace benefit, this idea is evolving. With the recent passage of the SECURE 2.0 Act, emergency savings accounts will be widely available from employers across the country. There are exceptions depending on your compensation level, so check with your benefits advisor or financial professional to understand your situation if your employer offers this benefit.

How healthy are you and your family?

If you're expecting to have notable healthcare costs in the year ahead—either for good reasons like pregnancy or challenging ones like a chronic condition—use open enrollment to review your current coverage and determine what you paid for premiums and copays during the year.

A health savings account, or HSA, could be a good option because it allows you to save and invest money tax-free if you combine it with a high-deductible medical insurance plan and spend any withdrawals on medical expenses. Because of their unique tax advantages, HSAs may also be a great way to save for retirement, as long as you invest the money inside your account and don't need to spend it in the shorter term for medical care.

If you're expecting higher medical costs in the upcoming year, most employers offer another type of plan called a flexible spending account, or FSA, which allows you to save for short-term costs. The money you put in an FSA is tax-deferred both at deposit and withdrawal as long as you spend it on medical costs. The only catch is that, unlike with an HSA, you must spend all the money you put into an FSA before the end of the benefit year or you'll lose it.

If you're still unsure which way to go, contact the human resources team at your employer so they can help answer your questions.

Who depends on you?

If something happens that makes you unable to work, it likely will have a financial impact not only on you but also on your parents, siblings, spouse and children. Disability insurance covers this potential crisis, and life insurance does the same in case of your death.

"We're three times more likely to become disabled than die," Sullivan says. "People talk about life insurance more than disability insurance, but it's important to analyze, understand and consider purchasing your employer's disability policy. And if their plan doesn't suit your needs, consider purchasing individually."

If your employer offers it, also review whether long-term care insurance makes sense.

What are your long-term goals?

Retirement tops the list for most employees. Fortunately, most employers support your path to this goal.

Traditional 401(k)s, for example, let you invest tax-deferred contributions that can grow tax-deferred until you withdraw it, preferably in retirement. Roth 401(k) contributions are taxed in the current year but grow tax-free and can be withdrawn tax-free. Many employers offer to match your contributions up to a certain percentage of your income.

Compound interest is the eighth wonder of the world, Harris says—and employer-matching contributions to your 401(k) aren't far behind. "If you're starting out, take the match, automate a 10% contribution from your starting salary, for example, and just behave like your compensation is actually 10% less a year," he says. "As you get a bit more established, increase this contribution by at least an annual percentage point. Not funding or funding below the match minimum is leaving free money on the table that could be compounding."

Other goals may be on your list as well, like buying or renovating a home, building a college savings fund or getting a different car. This brings up a common dilemma Harris sees with clients—whether to focus on paying down debt or working toward goals.

His answer is based on the loan terms and interest rate. "Student loans with interest below 6% can be paid off as scheduled, but accelerate paying on high-interest consumer debt like credit cards," he advises.

The bottom line

Answering these questions should help make the many small decisions you have easier as you go through open enrollment season. And if you need a bit more help to sort out the process, reach out to your financial advisor.

Insights

A few financial insights for your life

How to take full advantage of a pay raise

Don't fear employment credit checks