Creating an HOA emergency preparedness response plan

When a disaster strikes, having a clear emergency response plan in place can help protect people and property. In fact, disaster preparedness is a crucial responsibility of homeowner associations, or HOAs.

This guide outlines the key roles and responsibilities of HOA boards in disaster preparedness and provides best practices for creating and implementing an emergency response plan. It also covers post-planning steps, along with financial considerations for building HOA emergency savings to help avoid special assessments.

Responsibilities of an HOA

Disaster preparedness starts with a clear understanding of an HOA's role in developing and executing a response plan. While an HOA board is ultimately responsible, there are resources that can provide guidance and support, such as a community association management company.

The HOA board's role in disaster preparedness

The HOA board is responsible for making key decisions, communicating them and ensuring that the response plan is created and followed.

"The buck stops with the board," says Christi Wells, Director of National Accounts at First Citizens.

Boards have a fiduciary duty to protect common areas and ensure resident safety—and that includes being prepared for disasters.

Creating an emergency response plan

Before an HOA board creates a response plan, it's crucial to take the time to identify specific threats and consider the unique needs of the community. These first steps lay the groundwork for an effective strategy.

1Identify the likely risks

When creating an HOA emergency preparedness response plan, assess the specific risks your community is most likely to face. These could be natural disasters like hurricanes, floods or wildfires, or man-made events like civil unrest.

"Disaster plans aren't one-size-fits-all," Wells says. "You need to be prepared for Mother Nature and other unexpected events."

Understanding the risks that are most common to your location will help shape your plan.

2Consider the unique needs of your community

Every community has unique needs, and these must be factored into the disaster plan.

"Know your community and what it needs," says Cynthia Burns, Regional Sales Officer at First Citizens.

This includes considering vulnerable populations such as seniors, residents with physical limitations and pets.

"A lot of community associations have residents 55 and over," says Nicole Skaro, Vice President and Relationship Sales Officer for First Citizens. "So you could be talking about physical limitations but also monetary limitations because there may be people with fixed incomes."

3Understand your bylaws and local laws

An HOA emergency preparedness response plan must align with your association's governing documents, as well as local regulations.

"If you understand those two things right from the start, then you'll know to what level you should be involved," Skaro says.

Being familiar with these rules and regulations helps the board know what actions are required or allowed in the event of a disaster.

4Consider the type of development you live in

Different types of housing require different disaster preparedness measures. For example, high-rise buildings may need to focus on securing patio furniture and other items on balconies to prevent projectiles in a storm, while single-family homes might require residents to board up windows. Tailoring your plan to the specific requirements of the development you live in is key.

5Think about creating a disaster committee

If the HOA board feels overwhelmed, forming an emergency response team can help spread the responsibility. The committee can assist with planning, communication and organizing community-wide disaster drills.

6Conduct a reserve study

A reserve study helps evaluate the lifespan of your community's key components, such as common area buildings, landscape and infrastructure. The primary purpose of a reserve study is to estimate how much it will cost to replace these assets at the end of their expected useful life. However, the study may also provide critical insight into how much it would cost to repair or replace them earlier if a disaster causes irreparable damage.

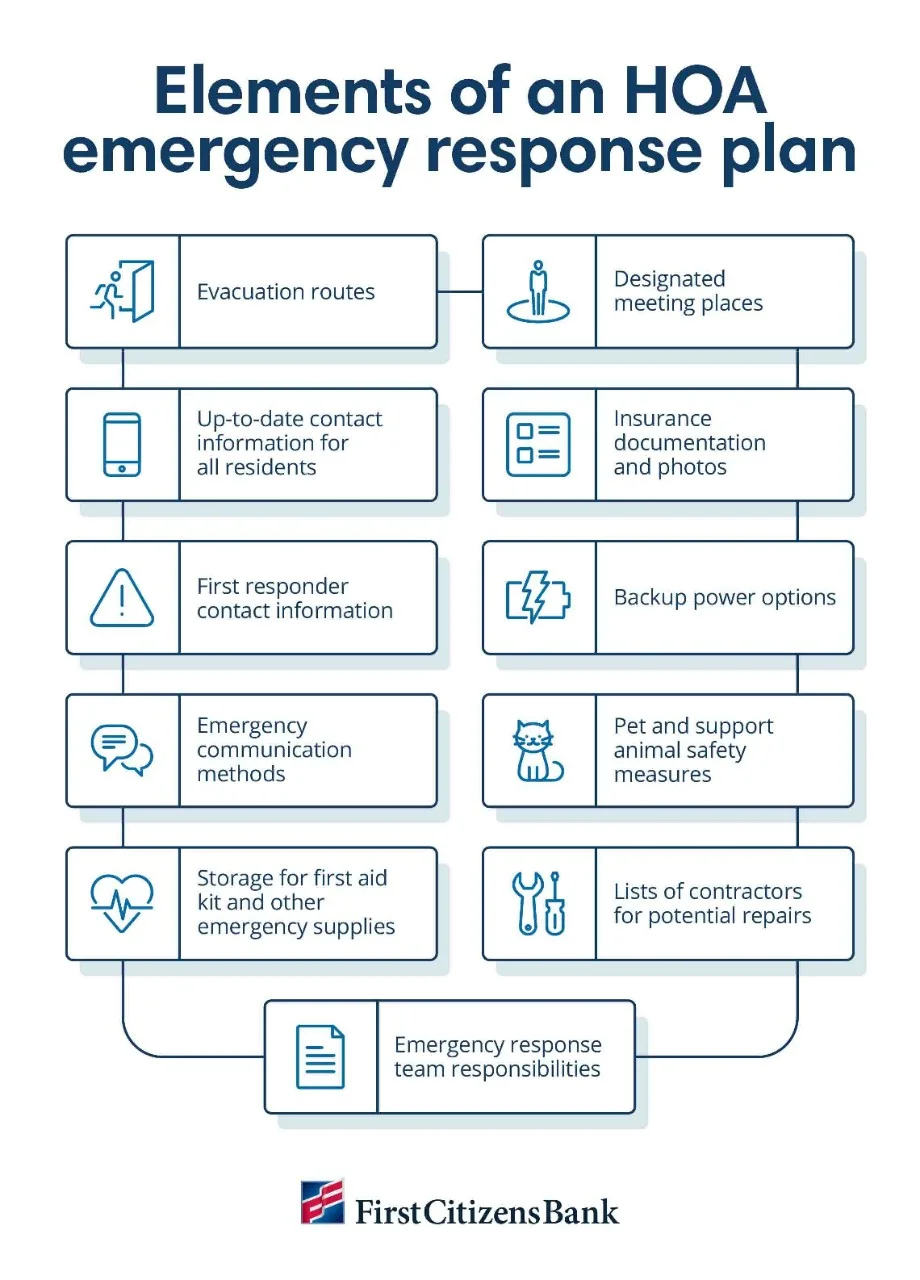

Key components of a plan

A comprehensive HOA emergency preparedness response plan should address various aspects to help ensure the community is equipped to respond to different types of disasters. From evacuation routes to essential contacts, these elements can help mitigate the impact and streamline the response process.

Maintaining and updating the plan

Once a community emergency response plan has been created, the next step is to make sure it can be implemented when needed. This involves clear communication, conducting drills and engaging with local experts to help keep the community prepared.

1Establish a communication plan

Ensure every resident knows what they should do during a disaster and how information will be shared.

"Sometimes we're too dependent on technology," Wells says.

A backup plan is critical in case of a power outage or cell service failure—common occurrences during a disaster.

2Engage local experts

Connect with local police, firefighters and emergency medical services personnel for safety reviews.

"They'll check fire alarms and offer guidance on evacuation routes," Skaro says.

Restoration companies, which clean and repair properties after a disaster, may also provide free disaster preparedness reports to identify potential risks.

3Conduct regular drills

Fire drills and disaster simulations are crucial for maintaining preparedness.

"Practice, practice, practice," emphasizes Wells, noting that periodic drills keep residents familiar with procedures and help ensure the plan works in a real scenario.

4Update the plan regularly

Emergency response plans should be reviewed and updated regularly to reflect any changes in the community's demographics or structural needs, or in the local laws.

Building an emergency fund

It may be costly to recover after a disaster—making financial preparation essential for an HOA. In fact, a best practice for HOA boards is to proactively set aside contingency funds that are earmarked for recovery.

One reason is that some states—or even the HOA's governing documents—may restrict using reserve funds for maintenance or repairs. Another reason is to avoid special assessments, which can create financial strain for residents.

"It can be really hard to communicate to residents that putting aside extra money in advance is for the greater good," Wells warns. "But that's part of the duty and care of being a fiduciary."

Rising insurance costs are another factor to consider. "Insurance premiums have in some cases gone through the roof," Skaro says.

HOAs need to plan to cover an insurance deductible and a possible insurance premium increase after a disaster.

How much should an HOA save for emergencies?

Ultimately, Wells recommends building up a cash cushion of at least 3 months of operating expenses, with another 6 to 9 months' worth in emergency savings.

"If you have the ability to raise assessments in a small incremental amount every year, the board should do that," says Wells. "To protect your community, it's important to have funds available when disaster strikes."

Gradual increases and dedicated contingency funds help keep an HOA prepared.

Still, if a disaster occurs and an HOA doesn't have adequate funds needed to recover, the board may be able to get a homeowners association loan. A bank that specializes in community association lending may offer financing that makes it easier to move forward without putting excess burden on homeowners or capital reserves.

The bottom line

For HOAs, disaster preparedness requires careful planning, clear communication and financial strategies. One essential step is to identify likely risks and assign roles and responsibilities from the start. Rising costs and legal obligations mean boards need to plan ahead and make informed decisions.

For guidance, reach out to a community association banker. They can work with you to ensure your community has the tools and resources it needs to prepare for the future.